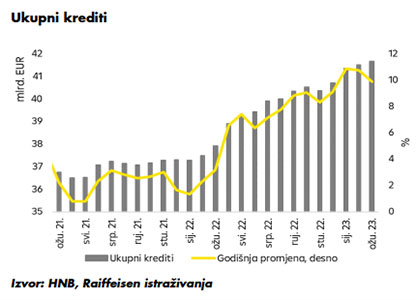

Krajem ožujka ukupni krediti 41,7 mlrd. eura

11.05.2023

Prema posljednjim podacima HNB-a, ukupni krediti drugih monetarnih financijskih institucija institucionalnim sektorima iznosili su na kraju ožujka 41,7 mlrd. eura, što je povećanje za 151,8 mil. eura ili 0,4% na mjesečnoj razini i 3,7 mlrd. eura ili 9,9% u odnosu ožujak 2022. (na osnovi stanja).

Promatrano po sektorima, krediti nefinancijskim poduzećima ukupnog iznosa 14,0 mlrd. eura bili su na kraju ožujka veći tek za 33,7 mil. eura ili 0,2% na mjesečnoj razini. Godišnja stopa rasta nastavila je usporavati, a u ožujku se spustila na 15,2% (+1,8 mlrd. eura) u odnosu na 20% zabilježenih u veljači 2023. Na godišnjoj razini, rast kredita za obrtna sredstva usporio je na 7,1% (+287 mil. eura), što je 8,5 postotnih bodova manje u odnosu na godišnju promjenu u veljači. Prva je to jednoznamenkasta stopa rasta ove kategorije u posljednjih godinu dana.

Krediti za obrtna sredstva na kraju ožujka iznosili su 4,3 mlrd. eura, a na mjesečnoj razini pali su za 1% ili 44,9 mil. eura. Istovremeno su krediti za investicije zabilježili rast za 50,7 mil. eura ili 0,9% u odnosu na veljaču, a iznosili su 5,6 mlrd. eura pri čemu je godišnja stopa rasta usporila s 16,2% u veljači na 13,6% u ožujku (+670,4 mil. eura).

S druge strane, krediti kućanstvima s iznosom od 20,1 mlrd. eura ostvarili su solidan rast u odnosu na veljaču (+1% ili 202,9 mil. eura), dok je u odnosu na ožujak 2022. rast iznosio 1,1 mlrd. eura ili 5,5%. Promatrano prema strukturi, stambeni krediti na koje se odnosi polovica ukupnih kredita plasiranih kućanstvima, s iznosom od 10 mlrd. eura, na mjesečnoj su razini ostvarili skroman rast od 0,5% ili 54,3 mil. eura.

U odnosu na ožujak 2022. stambeni krediti bili su viši za 866 mil. eura ili 9,5%. Intenzivniji rast stambenih kredita očekuje se u idućim mjesecima uslijed novoga kruga subvencioniranja stambenih kredita. Druga najveća stavka, gotovinski nenamjenski krediti, s udjelom od 36,6% u ukupnim kreditima kućanstvima i iznosom od 7,4 mlrd. eura, zabilježili su mjesečni rast od 1,4% (+103,2 mil. eura) te rast na godišnjoj razini od 3,3% (234,7 mil. eura).

Krediti općoj državi, od kojih se glavnina (87%) odnosi na kredite središnjoj državi, na kraju ožujka iznosili su 7,1 mlrd. eura. Uz povećanje u odnosu na ožujak prošle godine za 837,3 mil. eura (+13,4%), u odnosu na veljaču zabilježen je pad za 130,6 mil. eura ili 1,8%. Pri tome se većina kredita središnjoj državi odnosilo na dugoročne kredite (s dospijećem višim od 5 godina).

Na osnovi transakcija ostvaren je rast ukupnih kredita za 0,9% ili 0,3 mlrd. eura, prvenstveno kao odraz pojačanje kreditne aktivnosti sektora stanovništva (0,2 mlrd. eura ili 1,1%). Ubrzanje rasta gotovinskih nenamjenskih kredita može odražavati povećanu potrebu financiranja tekuće potrošnje u okružju ustrajnih inflatornih pritisaka i posljedičnog utjecaja na raspoloživi dohodak kućanstava. Rast bilježi i kreditiranje nefinancijskih poduzeća i ostalih nebankovnih financijskih institucija. U strukturi kredita nefinancijskim poduzećima, u odnosu na veljaču porasli su krediti za investicije, a smanjili se krediti za obrtna sredstva. Usporavanje godišnje stope rasta kredita nefinancijskim poduzećima odraz je i već snažnog rasta promatranih kredita u ožujku godinu dana ranije.

Disclaimer

Published by Raiffeisenbank Austria d.d. Magazinska cesta 69, 10000 Zagreb, Hrvatska (“RBA”). RBA is a credit institution and is has been incorporated in keeping with the Credit Institutions Act.

Economic Research and Financial Advisory are organizational units of RBA.

Supervisory Authority: Hrvatska agencija za nadzor financijskih usluga, Miramarska 24b, 10 000 Zagreb (Croatian Financial Services Supervisory Agency) and Hrvatska narodna banka, Trg hrvatskih velikana 3, 10 002 Zagreb (Croatian National Bank).

This publication is for information purposes only and may not be reproduced, translated, distributed or made available to other persons other than intended users, in whole or in part, without obtaining prior written permission of RBA on a case to case basis. This document does not constitute any kind of investment advice or a personal recommendation to buy, hold or sell financial instruments and it is neither an offer nor a solicitation of an offer. This document is not a substitute for any form of a legal document which is required pursuant to regulations of any state, including the Republic of Croatia, for a primary issue or secondary trading in financial instruments, regardless of whether investors are classified as retail or professional investors and regardless of whether they are entities or residents of the Republic of Croatia or of any other jurisdiction.

This publication is fundamentally based on generally available information, which we consider to be reliable, but we do not make any representation, warranty or assurance as to accuracy, completeness or correctness of such information. All analyses contained in this publication are based solely on generally available information and on assumption that the information is complete, true and accurate, which may not necessarily be the case, and, for the user, they involve risks related to issuer, capital market, general economic and political environment and prospects. The estimates, projections, recommendations or forecasts of future events and opinions expressed in this publication constitute independent judgement made by analysts as at the date of publication, unless explicitly otherwise stated. The following sources were material for the preparation of this publication: the Croatian Bureau of Statistics, the Croatian National Bank, the Government of the Republic of Croatia, the Croatian Employment Service, the Croatian Pension Insurance Institute, the Ministry of Finance, the Croatian Financial Services Supervisory Agency, the Zagreb Stock Exchange, the Institute of Economics, Bloomberg, Eurostat, the Vienna Institute for International Economic Studies and other sources which are expressly stated in the analysis.

RBA is under no obligation to keep current the contents of this publication and reserves the right to withdraw or suspend them in whole. The publication of an up-to-date revised analysis, if any, shall be made at the discretion of analysts and RBA. In case of any modification or suspension of the contents of this publication, RBA shall publish the notice of modification or suspension, and information regarding the circumstances which lead to the modification or suspension of this publication, in the same manner as this publication, with a clear reference to the fact that the modification or suspension apply to this publication.

This publication does not purport to be and does not constitute a basis for making any investment decision and all users are advised to seek additional expert advice and information to the extent they deem necessary, before making any investment decision.

The prices of financial instruments mentioned in this publication are the closing prices available at 16:30 CET on the day which precedes the date of this publication, unless stated otherwise in the publication.

Investment options discussed in this publication may not be appropriate for certain investors, depending on their specific investment objectives and investment time horizon, and taking into account their overall financial situation. Investments which are the subject of this publication may vary in price and value. Investors may generate returns which are below their initial capital investment. Exchange rate changes may adversely affect the investment value. Besides, past performance is not indicative of future results whatsoever. Risks arising from investment in financial instruments, financial products or investment instruments which are the subject of this publication are not explained in whole or in full detail. Information is provided “as is” without giving warranties of any kind and may not be deemed to substitute any investment advice. Investors have to make independent decision regarding the appropriateness of investment in any instruments discussed or mentioned in this document, based on risks and benefits resulting from such instruments, and on their investment strategy and legal, fiscal and financial position. As this publication is not personal recommendation for investment, neither it and nor any of its components, forms a basis for conclusion of any kind of deal, contract or commitment whatsoever, nor should it be relied upon or used as an incentive for or in connection with such actions. Investors are advised to seek specific detailed information and advice from competent certified investment advisors.

RBA, Raiffeisen Bank International AG ("RBI"), and any other company connected with them, including their directors, authorized representatives or employees, and any other party, do not accept any responsibility of liability arising in any way (whether due to negligence or otherwise) for any damages or losses whatsoever which result from the use of this publication or its contents or which may otherwise be caused in connection with this publication.

This publication is disseminated to investors who are expected to make independent investment decision and estimates of investment risks, including issuer risk, capital market risk and risks related to economic and political circumstances and prospects, without placing undue reliance on this publication, and this publication shall not be distributed, reproduced or published in whole or in part for any purpose, without RBA's permission.

RBA publishes financial instrument valuation and analyses independently or as part of publications which are created and distributed by RBI and Raiffeisen Centrobank, Austria ("RCB") under the name Raiffeisen ISTRAŽIVANJA. The analyses may relate to one or more issuers, and to financial instruments issued by them.

Unique criteria for issuance of stock market recommendation (rating) and risk classification are defined as follows:

„Buy“: for stocks which have an expected total return at least 10% (15% for stocks with high volatility risk) and represent the most attractive stocks among all stocks we analyze and valuate over next 12 months

„Hold“: for stocks for which we expect a positive return up to 10% (up to 15% for stocks with high volatility risk) over next 12 months.

„Reduce“: expected negative return up to -10% over next 12 months.

„Sell“: for stock with expected negative return by more than -10% u over next 12 months.

Target prices are based on calculated fair value which is derived by applying relative valuation tools (peer group analysis) or discounted cash flow DCF method. Detailed information on specific valuation methods applied is available at:

https://equityresearch.rbinternational.com/concepts.php

When publishing the analyses, ratings are determined by applying above mentioned ranges. Temporary deviations from the aforementioned ranges will not automatically result in the alteration of a recommendation, and the respective recommendation will be placed under review instead.

Opinions concerning Croatian money market rates and price fluctuations of government bonds issued in the Republic of Croatia are based on the analysis of market ratio movements.

This publication is not an offer or a personal recommendation to buy or sell a financial instrument. Information presented here does not constitute a comprehensive analysis of all material facts related to issuer, industry or financial instrument. This publication may contain expectations and forward-looking representations, which involves risks and uncertainties, however, they are not a warranty or indication of future results whatsoever and are therefore subject to change. Therefore, no warranty or representation, whether express or implied is made and no reliance should be placed on the fairness, accuracy, completeness or truth of information and views provided in this publication.

RBA analysts are involved in production of recommendations published and distributed by RCB, regarding the companies listed below along with the date of initial recommendation:

- Adris Grupa d.d. (21.01.2005.), Atlantic Grupa d.d. (8.6.2015.), Ericsson Nikola Tesla d.d. (18.01.2005.), Hrvatski Telekom d.d. (11.12.2007.), Ledo d.d. (13.10.2015.), Podravka d.d. (3.3.2003.) i Valamar Riviera d.d. (17.12.2015.).

Overview of Raiffeisen recommendations:

|

| Buy | Hold | Reduce | Sell | Suspended | Under review |

| No. of recommendations | 1 | 4 | 1 | 0 | 1 | 0 |

| % of all recommendations | 14% | 58% | 14% | 0% | 14% | 0% |

| Investment banking services | 0 | 0 | 0 | 0 | 0 | 0 |

| % all IB services | 0% | 0% | 0% | 0% | 0% | 0% |

A list of all historic recommendations for stock coverage, local money market rates in the Republic of Croatia, Croatian government bonds issued in the local markets and other recommendations is available at:

http://www.rba.hr/istrazivanja/povijest-preporuka

Please note that RBA, its related companies, employees, executives and other persons who participated in the preparation of this publication, and their related persons, may hold or trade in financial instruments in excess of 0.5% of the issuer's equity stake or deal with entities from the industries discussed in this publication. However, by applying confidentiality protection and conflict of interest prevention measures RBA has ensured to a reasonable extent that this circumstance has not in any way affected anything that is mentioned in this publication.

RBA is part of RBI Group. RBI is a business investment bank domiciled in Austria. For 25 years RBI has been active in Central and Eastern Europe (CEE region) where it operates a network of subsidiary banks, leasing companies and numerous other companies which provide financial services in 17 markets. As a result of its position in Austria and CEE, RBI has established relationship, or expanded them in some cases, with companies in the following industries: oil & gas, technology, energy, real estate, telecommunications, financial services, core materials, cyclical and non-cyclical consumer goods, healthcare and industry. RBI and/or its related companies executed transactions related to products and services (including, but not being limited to, investment banking services) with the issuer mentioned in the analysis during the past 12 months. RBI and related companies have set up organizational measures which are required from the legal and supervisory point of view, and the implementation of the measures is monitored by the Compliance. Conflicts of interest are subject to application of legal, physical and other restrictions (referred to collectively as the Chinese Walls), the purpose of which is to contain the flow of information between business lines/organizational units within RBI, RBA, RCB and other group members. So for instance, Investment Banking, which comprises corporate funding activities through capital markets is separated by physical and other barriers from the front office and from research and analysis units.

Potential conflicts of interest listed below will apply to financial instruments discussed in the analysis if their respective numbers are indicated at the end of the chapter:

1. RBA or any related company or any private individual involved in the publication of this document owns a net long or short position exceeding the threshold of 0,5 % of the total issued share capital of the issuer.

2. Holdings of the issuer in the total issued share capital of the RBA or any related company exceed 5 %.

3. RBA or any related company or any individuals involved in the publication of this document hold significant financial interests in relation to the issuer.

4. RBA or any related company act as market maker or liquidity provider in the financial instruments of the issuer, where applicable.

5. RBA or any related company has been lead manager or co-lead manager over the previous 12 months of any publicly disclosed offer of financial instruments of the issuer, in terms of underwriting the offer or sale of financial instruments of the issuer with or without repurchase, where applicable.

6. RBA or any related company is party to any other agreement with the issuer relating to the provision of investment banking services, provided that this would not entail the disclosure of any confidential commercial information and that the agreement has been in effect over the previous 12 months or has given rise during the same period to the payment of a compensation or to the promise to get a compensation paid, where applicable.

7. RBA or any related company or any individuals involved in the publication of this document is party to an agreement with the issuer relating to the production of the recommendation, where applicable.

8. Analysts or any individuals involved in the publication of this document hold the financial instruments of the issuer which he or she has analyzed.

9. Analysts or any individuals involved in the publication of this document sit on the Supervisory Board/Board of Directors of the issuer analyzed by him or her.

10. Analyst or any individuals involved in the publication of this document have received or acquired the financial instrument of the issuer prior to the public offering of the issue. In this case the transaction has to be pre-approved at a disclosed date and buy or sell price.

11. The remuneration of analysts or any individual involved in the publication of this document is tied to the provision of investment banking service by RBA or any related company.

Applicable notes: Note 3, 4 and 5.

Portfolios of analysts and other individuals who participated in the creation of this analysis are available at: http://www.rba.hr/istrazivanja/portfelj-rba-analiticara

Analyst statement: Remuneration of the analyst is and shall not be tied, directly or directly, to the recommendations or views presented in this publication, nor shall it depend on executed transactions.

RBA employee who has not been involved in the preparation of this publication, but had access to it, prior to its distribution, has no significant financial interest in one or more financial instruments of the issuers discussed in the publication. RBA employee who has not been involved in the preparation of this publication, but had access to it, prior to its distribution, is not deemed to be in the conflict of interest in relation to the issuer discussed in the publication.

RBA has received license from the Croatian Financial Services Supervisory Agency (“HANFA”) for performance of all activities governed by the relevant Capital Markets Act and other applicable rules and regulations. However, RBA is only authorized to perform these activities on the territory of the Republic of Croatia and not elsewhere. In case this publication or any part of it should become available in any jurisdiction other than the Republic of Croatia, it should be deemed to be nonexistent.

SPECIAL REGULATIONS FOR THE UNITED KINGDOM OF GREAT BRITAIN AND NORTHERN IRELAND (UK): This document does not constitute either a public offer in the meaning of the Austrian Capital Market Act (Kapitalmarktgesetz; hereinafter „KMG“) nor a prospectus in the meaning of the KMG or of the Austrian Stock Exchange Act (Börsegesetz). Furthermore, this document does not intend to recommend the purchase or the sale of securities or investments in the meaning of the Austrian Supervision of Securities Act (Wertpapieraufsichtsgesetz). This document shall not replace the necessary advice concerning the purchase or the sale of securities or investments. For any advice concerning the purchase or the sale of securities of investments kindly contact your RAIFFEISENBANK. This publication has been either approved or issued by RBI in order to promote its investment business. Raiffeisen Bank International AG (“RBI”), London Branch is authorised by the Austrian Financial Market Authority and subject to limited regulation by the Financial Conduct Authority (“FCA”). Details about the extent of its regulation by the FCA are available on request. This publication is not intended for investors who are Retail Customers within the meaning of the FCA rules and shall therefore not be distributed to them. Neither the information nor the opinions expressed herein constitute or are to be construed as an offer or solicitation of an offer to buy (or sell) investments. RBI may have affected an Own Account Transaction within the meaning of FCA rules in any investment mentioned herein or related investments and/or may have a position or holding in such investments as a result. RBI may have been, or might be, acting as a manager or co-manager of a public offering of any securities mentioned in this report or in any related security.

SPECIFIC RESTRICTIONS FOR THE UNITED STATES OF AMERICA AND CANADA: This document may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada, unless it is provided directly through RB International Markets (USA) LLC (“RBIM”), a U.S. registered broker-dealer, and subject to the terms set forth below.

SPECIFIC INFORMATION FOR THE UNITED STATES OF AMERICA AND CANADA: This research document is intended only for institutional investors and is not subject to all of the independence and disclosure standards that may be applicable to research documents prepared for retail investors. This report was provided to you by RB International Markets (USA) LLC (RBIM), a U.S. registered broker-dealer, but was prepared by our non-U.S. affiliate Raiffeisen Bank International AG (RBI). Any order for the purchase or sale of securities covered by this report must be placed with RBIM. You can reach RBIM at 1133, Avenue of the Americas, 16th floor, New York, NY 10036, phone +1 212-600-2588. This document was prepared outside the United States by one or more analysts who may not have been subject to rules regarding the preparation of reports and the independence of research analysts comparable to those in effect in the United States. The analyst or analysts who prepared this research (i) are not registered or qualified as research analysts with the Financial Industry Regulatory Authority (“FINRA”) in the United States, and (ii) are not allowed to be associated persons of RBIM and are therefore not subject to FINRA regulations, including regulations related to the conduct or independence of research analysts.

The opinions, estimates and projections contained in this report are those of RBI only as of the date of this report and are subject to change without notice. The information contained in this report has been compiled from sources believed to be reliable by RBI, but no representation or warranty, express or implied, is made by RBI or its affiliated companies or any other person as to the report’s accuracy, completeness or correctness. Securities which are not registered in the United States may not be offered or sold, directly or indirectly, within the United States or to U.S. persons (within the meaning of Regulation S under the Securities Act of 1933 [“the Securities Act”]), except pursuant to an exemption under the Securities Act. This report does not constitute an offer with respect to the purchase or sale of any security within the meaning of Section 5 of the Securities Act and neither shall this report nor anything contained herein form the basis of, or be relied upon in connection with, any contract or commitment whatsoever. This report provides general information only. In Canada it may only be distributed to persons who are resident in Canada and who, by virtue of their exemption from the prospectus requirements of the applicable provincial or territorial securities laws, are entitled to conduct trades in the securities described herein.

EU REGULATION NO 833/2014 CONCERNING RESTRICTIVE MEASURES IN VIEW OF RUSSIA’S ACTIONS DESTABILISING THE SITUATION IN UKRAINE

Please note that research is done and recommendations are given only in respect of financial instruments which are not affected by the sanctions under EU regulation no 833/2014 concerning restrictive measures in view of Russia's actions destabilising the situation in Ukraine, as amended from time to time, i.e. financial instruments which have been issued before 1 August 2014.

We wish to call to your attention that the acquisition of financial instruments with a term exceeding 30 days issued after 31 July 2014 is prohibited under EU regulation no 833/2014 concerning restrictive measures in view of Russia's actions destabilising the situation in Ukraine, as amended from time to time. No opinion is given with respect to such prohibited financial instruments.

INFORMATION REGARDING THE PRINCIPALITY OF LIECHTENSTEIN: COMMISSION DIRECTIVE 2003/125/EC of 22 December 2003 implementing Directive 2003/6/EC of the European Parliament and of the Council as regards the fair presentation of investment recommendations and the disclosure of conflicts of interest has been incorporated into national law in the Principality of Liechtenstein by the Finanzanalyse-Marktmissbrauchs-Verordnung.

If any term of this Disclaimer is found to be illegal, invalid or unenforceable under any applicable law, such term shall, insofar as it is severable from the remaining terms, be deemed omitted from this Disclaimer. It shall in no way affect the legality, validity or enforceability of the remaining terms.